Use The Zebra’s car insurance calculator to quickly and easily estimate how much your auto insurance could cost in your area. Enter your ZIP code to get started or read more.

Tips for getting an accurate estimate

💡 Provide accurate information. It’s crucial to provide accurate information, whether you use a calculator or get a formal quote from a comparison tool. Customers are often shocked at how details they perceive as “small” affect their final rate.

💡 Take time to understand your coverage options. Choose the ones that best suit your needs and budget, and don’t skimp on coverage to save money up front. We’ll discuss coverage more later on.

💡 Take the next step and get a quote! We aren’t saying this just because we’re an insurance comparison site: an insurance quote provides more personalized, accurate pricing as it considers more factors.

“Insurance calculators are designed to provide quick, generalized estimates. This is why people often see a discrepancy between a rough estimate and a more detailed quote. Calculators are an excellent starting point, however, they’re just not as accurate as a quote from our comparison engine or one finalized by one of our agents.”

How car insurance premiums are calculated

Car insurance companies consider various factors in a driver’s profile to determine rates, some within their control—like good driving record or driving an affordable car— and some aren’t.

Rates are also influenced by location, age, gender, marital status, credit score, vehicle, and driving history. Lower risk results in lower premiums. Let’s explore these rating factors and their impact on your car insurance premium.

Insurance companies assess applicants by certain demographics to gauge risk and assign appropriate insurance rates:

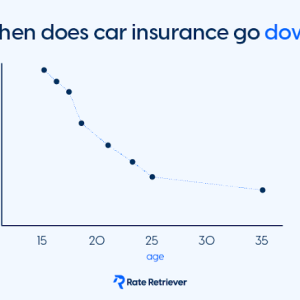

- Age

- Credit score

- Marital status

- Gender

- State regulations: Each state sets its own insurance requirements, which can impact pricing. States with higher minimum coverage or PIP requirements often have higher premiums.

- ZIP code pricing: Insurers use your ZIP code to assess risk. Areas with more drivers or higher risks (like theft, vandalism, or natural disasters) tend to have higher rates.

One of the most important risk factors insurance companies assess is your driving history:

- Past tickets, accidents, or violations suggest higher risk and usually lead to more expensive premiums.

- Gaps in coverage can raise red flags. Insurers prefer drivers with continuous coverage and higher limits, which signal financial responsibility.

- Sports cars and newer models typically cost more to insure due to repair costs. Rates can also vary based on whether your car is owned, leased, or financed.

More protection means a higher premium—but also more financial security if you need to file a claim.

- Higher coverage limits increase your premium because your insurer is responsible for paying out more in a claim.

- Liability vs. full coverage: Full coverage includes comprehensive and collision insurance, which significantly raises the cost compared to a liability-only policy.

- Opting for a higher deductible can lower your premium, but you’ll pay more out of pocket if you’re in an accident.

Understanding how much car insurance you need

Determining how much car insurance coverage you need depends on various factors, such as your state’s minimum requirements, your vehicle’s value, your financial assets, your risk tolerance, and, when applicable, your lender. It’s important to consider coverage for liability, collision, comprehensive, uninsured/underinsured motorist, medical payments, and personal injury protection.

🛡️ State minimum: Only includes liability coverage (property damage and bodily injury) and possibly state-specific coverages like PIP or UMBI; liability pays the other driver in the event of an accident and is the lowest (and cheapest) level of coverage available. It does not offer a lot of protection but is legally compliant.

Best for: drivers with vehicles worth less than $4,000

🛡️ Full coverage: Includes liability, comprehensive and collision coverages, as well as any other state-specific required coverages. Comprehensive and colllision each come with a deductible, which you can set (higher deductibles typically mean lower monthly premiums).

Best for: Drivers with financed or leased vehicles or those who prefer high levels of protection.

How to save on car insurance premiums

While rating factors do exist and are difficult to change, there are a few steps you can take to make sure you are getting the best rate possible for your situation.

Compare quotes

The best way to save on car insurance premiums is by comparing quotes at each renewal period.

Look for discounts

Most insurance companies offer discounts for which you may qualify. If you have multiple insurance policies, bundling offers excellent savings.

Choose an affordable vehicle

Typically, cars with lower costs of repair tend to have cheaper insurance rates.