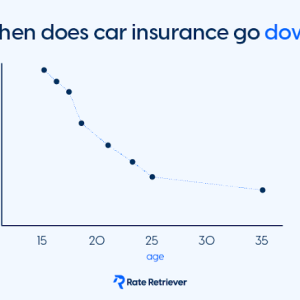

Generally speaking, you should compare car insurance quotes every six months to make sure you’re with the right insurance company. Even if nothing changes with you, your rates could go up for a number of reasons during that timeframe. However, there are a few life events that could qualify you for cheaper rates that include moving to a new state, adding a new vehicle to your policy, getting married and even getting older.

If you find a cheaper rate elsewhere (ideally for the same coverage), cancel your current policy and move on to the new insurer as soon as you can. For most companies, the process to cancel is very straightforward. Depending upon how much time you have left in your auto insurance policy, the remaining premium can be refunded back to you.

Use car insurance discounts

Some car insurance discounts are automatically added to your auto insurance quote when they pull your driving report, but you should always make sure they’re not missing anything. Below are some potential discounts and cost-cutting programs in which you can participate to help get you the cheapest quote.

- Auto-pay discount

- Good driver discount

- Multi-driver discount

- Multi-vehicle discount

- Paperless billing discount

- Senior discount

- Student discount

- Telematics programs

Change your deductible

A general rule in the insurance world is if the vehicle you own is worth less than $4,000, you can consider dropping collision and comprehensive (i.e. full coverage) insurance. The reasoning is simple: the after-market value of your vehicle isn’t worth the cost to insure it. However, if you’re like the 50% of our customers that lease or finance your vehicle, you’re usually required to keep full coverage. If it’s necessary for you to have full auto insurance coverage but you want to save money, consider adjusting your deductible.

Because your car insurance deductible and premium are inversely related, you can lower your bill by raising your deductible. Looking at the chart below, you can see how your premium will change with a $500 and $1,000 deductible.[2]

Quotes comparison example

After receiving numerous car insurance quotes, a price-minded shopper has narrowed down their options to the three below. Cost is a major consideration, but the customer also wants to make sure they have comprehensive and collision coverage to add further peace of mind. Based on the information presented, which quote do you think they should choose?

Note that the format for liability coverage is X/Y/Z where:

- X = bodily injury/person

- Y = bodily injury/accident

- Z = property damage/accident

All three options were close in price, but #1 offered less liability coverage. Between #2 and #3, the only real difference was in the deductible, which was more expensive for the third option. Because this customer isn’t overly concerned about a higher deductible

-

Information needed to get insurance quotes

In order to receive a car insurance quote, you’ll need to have the same basic information handy. To speed up the process, make sure have the following ready to share:

Driver’s license

Driver’s licenseName, address (or your vehicles garaging location), and birthday are required in addition to gender and marital status. Some insurance companies will also require your Driver License number.

Vehicle type

Vehicle typeYou need to know the year, make, model, and trim of your primary vehicle. While you don’t need to know your vehicle identification number (VIN) during your quoting stage, you will eventually need it to buy your policy.

Other vehicle details

Other vehicle detailsVehicle status (owned or leased), primary use and average miles driven are typically asked for as well.

Insurance history

Insurance historyHave you had continuous coverage or are you currently uninsured? Some car insurance companies require at least six months of continuous auto insurance to issue a policy.

Additional information

Additional informationLastly, you’ll be asked about any accidents or citations (excluding parking tickets), so having a clean driving record is ideal. Credit score and highest-level of education will also be needed to understand what kind of risk you might be.